Price pressures build for Engineering Polymers whilst some other polymer prices moderate.

The buying frenzy in April, which resulted from availability concerns following the US/Iran conflict and the closure of the vital Strait of Houmous shipping route, may have resulted in the price of some standard polymers overshooting and as a consequence, there have been some minor pricing corrections in May.

It is notable that significant quantities of product were released onto the market, often at discounted prices, probably based upon material that was produced and purchased prior to the recent crisis. These additional volumes serve to further confuse the fundamentals of the market in terms of supply and demand and, in any case, given that Brent Crude Oil is forecast to trade above $100 per barrel for the rest of 2026, then it will be difficult to envisage polymer prices returning to the levels seen at the beginning of this year. A more likely scenario is that prices will plateau, possibly around the current levels for standard polymers.

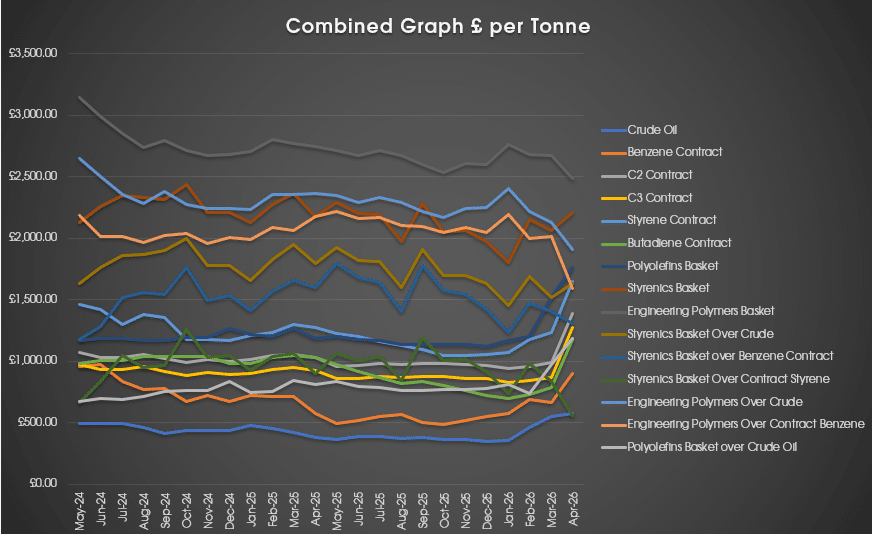

As depicted in the graph below, inflationary pressures in the form of input costs, along with a downward trend in market prices for many polymer types are eroding the profit margins for producers of Engineering Plastics. Although demand for the consumer durables, which constitute a dominant area of demand for these materials, will be stifled by the geopolitical uncertainty resulting from the conflict in the Middle East, producers are already starting to announce significant price increases in an effort to recover profitability.

Whilst a resolution to the conflict would be a welcome relief to many, it is notable that supply chain disruption of which more is likely to come, may last well into the rest of 2026 and possibly beyond. Although not entirely desirable, it is better to have expensive polymer rather than no polymer at all.

Monomer Price Movement

Feedstock

Price per Tonne

Change (contract)

C2 (Ethylene)

£1,475.93

£87.08

C3 (Propylene)

£1,380.15

£104.49

SM (Styrene Monomer)

£1,695.36

£47.89

Benzene

£926.48

£27.86

Butadiene

£1,197.29

£174.15

Brent Crude (monthly average)

£573.85

£23.73

Exchange Rates

€

1.15

$

1.36

€/$

1.18

Mike Boswell Executive Chairman – Plastribution Group

May has seen prices broadly flat with some European producers still pushing for increases reflecting the monomer movement whilst some more import dependent grades are seeing slight reductions. C2 and C3 rose by €100 and €120 / MT respectively and whilst some PP is seeing that passed through, the PE market looks more balanced and the increases way beyond monomer in April have impacted demand.

Whilst imports from the Middle East continue to be severely restricted, we are seeing US imports of PE replace them, but PP is more difficult to substitute and that is keeping prices up

Styrene Monomer is up €55 / MT over April, and the market is passing that through. Availability is restricted, particularly on HIPS with FM in place at Trinseo.

Outlook beyond May is for relative stability, whilst price reductions are welcome, we are unlikely to see anything significant to offset the April increases for some time. We are still seeing shortages on all grades and major challenges in getting product out of the Middle East. We are starting to see the impact of a lack of raw material heading to SE Asia.

There is some expectation that raw material costs will drop in the summer as we hopefully see the coflict resolved and oil prices drop but it continues to be a volatile situation.

LDPE has broadly rolled over in May. Although monomer increased €100 / MT, this has been absorbed by producers who saw much improved margins in March and April. Availability is better this month as SABIC are no longer in FM, though there are still some issues in production throughout Europe.

LLDPE

Supply

Demand

LLDPE is rollover to slightly down in May. Panic buying has gone and with a more measured approach, offers for imported material are improving. Reductions are welcome but likely to be slight relative to increases seen already this year.

HDPE

Supply

Demand

HDPE is also rollover to slightly down though perhaps not by as much as LLDPE. We are more reliant on the Middle East for HDPE and whilst there is some coming from the US to help, availability is still restricted.

PP

Supply

Demand

PP pricing is a mixture, mostly depending on the end point of April. Some are targeting the full monomer, some accepting rollover and some falling in between. PP is a major export of the Middle East, and the other regions that import to Europe (SE Asia) cannot produce due to a lack of feedstock. PP market expected to stay tighter than PE as alternative sources are not as readily available.

PS

Supply

Demand

PS pricing has risen in line with the monomer increase of €55 / MT. Whilst demand is muted, imports are down and Trinseo are in Force Majeure on HIPS.

Other Polyolefins

EVA pricing is rollover to slightly up as VAM costs continue to rise. Higher VA content grades are more affected. Speciality POP and POE grades have mostly moved up with monomer this month

The market for performance polymers is still being dominated by events in the Middle East, particularly how it is affecting global supply chains. It remains to be seen just how much of a medium to long term impact it will have, but for now, the messaging is one of higher prices, longer lead-times, and continued shipping issues. With prices still rising in most cases, it looks likely that any stability is still some way off.

The Benzene contract price for May settled at €1064/t, up by a further €32/t from April, with availability also still impacted.

Pete Tillin Product Manager – Performance Polymers

Performance Polymer Feedstocks £/Metric Tonne by month

No Data Found

ABS

Supply

Demand

ABS prices are still rising, but the rate of increase has slowed. The styrene monomer contract price increased by a further €55/t in May, ACN was also up by €168/t, and butadiene up €200/t. Supply remains low, and many customers are now waiting to see what happens longer term, with much of the panic buying having already taken place.

PA6

Supply

Demand

Prices are still increasing at pace, with numerous announcements from producers, but demand is low, so no short-term supply issues are foreseen.

PA66

Supply

Demand

A similar picture to PA6, with further increases announced and implemented. However, demand is low, with many converters sitting tight until cheaper material from the Far East potentially starts to arrive.

POM

Supply

Demand

As with many other performance polymers, demand is down, however material is tight so producers continue to force through increases. This situation will only improve once availability/stocks get better

PC

Supply

Demand

Price rises continue, albeit at a slower rate. How much will be forced through depends on demand and the level of imported material, particularly from the Far East.

PMMA

Supply

Demand

Similar to other materials, prices are still rising but at a slower rate. Availability is starting to improve which may change how much producers can force through.

PBT

Supply

Demand

Supply is low, so producers are forcing through further price increases.

Other Engineering Polymers

The situation for all other engineering materials is broadly similar, with poor availability and increasing prices

Recycled Polyolefins are continuing to rise in price although the pace of increase is softening. As prime prices have corrected slightly down following the boom in April, the momentum has been lost a little bit. Availability of prime is still a concern so we should continue to see better demand for recycled grades and prices holding up. Remains to be seen what happens with new bale input pricing.

Recycled LDPE / LLDPE has seen further increases in May though not as strongly as in April. High quality “natural” grades are doing very well with demand now outstripping supply as buyers look for alternatives to €2,400 / MT prime LDPE. Whilst up, industrial grades are not increasing as strongly as supply and demand remain more balanced.

Recycled HDPE

Supply

Demand

Recycled HDPE continues to climb in price though not quite as strongly as we saw in April. Grades suitable for virgin substitution are in strong demand are trading at similar prices to virgin. More industrial grades are also in demand but supply remains strong and increases are more moderate.

Recycled PP

Supply

Demand

Recycled PP is up, natural grades for consumer packaging are close to virgin prices. Industrial grades for construction applications etc. are up though the picture is a little more balanced in supply and demand.

Contact Mike Boswell

Executive Chairman

Contact Ian Chisnall

Product Manager – Sustainable Polymers

Contact Pete Tillin

Product Manager – Performance Polymers

The latest updates sent straight to your inbox

Simply enter your details below to subscribe to Price Know-How